|

Learn and Become Independently Wealthy Being financially stable ensures you have enough funds that you will never need to work again to cover your bills or rely on others for financial assistance. Financial freedom is not the same as independent capital. Financially self-sufficient people do not depend on anyone to cover their bills; they have a stable income from work, a career, or passive income sources.  When you are financially independent, you not only pay your bills on your own, but you also don't need to work to supplement your salary. How much money do you require to be financially self-sufficient? This number is personal and subjective and is solely based on your life goals and ambitions. That could mean you have millions or a few hundred thousand dollars earning interest. It all depends on your preferred way of living. How Do Most People Perceive Independent Wealth?Are you a self-made millionaire because you own a Ferrari? Since they have myths about what independent capital is, most people believe it is unattainable. Can you picture someone who has made it as you hear of someone who:

How Many Millions Do You Need to Be Independently Wealthy?The bottom line is that you would have enough money to be financially independent without ever working. This does not imply that you would stop working; however, being financially independent allows you to do so. Your chosen way of life determines the sum you require. You can be close if you have enough funds to cover your bills without having to search for a monthly salary. You would build passive income to be able to live without having to work for a living. For instance, If your monthly investment income is $5,000 and your monthly spending is $3,500, you have already built independent capital. This ensures that you will go without working forever as long as the monthly spending does not increase. If you spend $3,500 a month on your budget, you'll need $42,000 a year. Most financial analysts believe that to be considered "independently rich," you must have at least 25 times your annual expenses–in this case, $42,000 multiplied by 25 equals $1.05 million. You can now budget for half the discretionary expenses, which may be as much as $60,000 a year. This implies that you'll require: 1,050,000 + (60,000 x 25) = $2,550,000 You'll need to invest up to $2.55 million or get an annual passive benefit of up to $102,000. You're still called "independently affluent" after that. How Do You Recognize You Have Independent Wealth?Developing self-sufficient capital necessitates perseverance and restraint. The definition of deferred gratification must be extended here, where you enjoy less now in order to enjoy more tomorrow. If you arrive, you will be able to tell if:

Why Focus on Building Independent Wealth?Want to know why one must focus on becoming independently wealthy? Check the benefits mentioned below. Freedom to Pursue Your DreamsYou will have the freedom to spend on what makes you happier until you have enough money or passive income to survive indefinitely without having to work. You would be able to do activities you like more than things you are obligated to do. For example, you can grow organic vegetables in your kitchen garden for a healthier lifestyle because you have the time. Make decisions that will serve you in the long run.Being individually wealthy gives you the right to make choices that will help you in the long run. You'll be making choices based on your imminent survival. This will also assist you in increasing your income by allowing you to escape debt. Change the way you think about money.If you have sufficient passive income to live comfortably, you will see money as merely a means to support others and live the life you want. The money would not be able to manipulate or determine who you are. You may also discover how wasteful it is to please people by wearing costly clothes or driving expensive cars. Get Peace and Relieve StressYou will be more at ease if you are debt-free and have sufficiently passive profits. Your financial situation will cause you less worry. When you don't owe someone else money, you can keep control of your finances and use them to support your interests and charities. You'll be able to concentrate on your health.Financial independence allows you to reclaim your time. You'll have more time to exercise and prepare nutritious foods, and you'll be able to concentrate on having an adequate sleep each night rather than rushing to your second job. You will spend your attention and resources on things that truly matter by concentrating on your wellbeing and relationships without the debt burden. True wealth entails a safe body, mind, and relationships in addition to income. Making Sacrifices to Become Wealthy on Your OwnBuilding wealth is a long and arduous process that necessitates sacrifice. The following are some of the items you will have to give up:

Easy Cash Flow Options Getting a side hustle is the simplest way to boost your profits. You can pick up a few new talents and use them on the side to supplement your income. These side hustles would allow you to supplement your income and put money into your savings account. Popular money-making side hustles include freelancing jobs that are common include:

Expert advisorYou can work as a manager on the side if you're good at what you do. People will seek your advice, and you will bill them for it. You will supplement your salary without taking on a side job by: Requesting a Pay IncreaseYour current job can allow you to earn more money each year. What would it be like to go from making $70,000 to $120,000 a year? It will increase your income and help you achieve your goal of being financially stable. You must, however, put in the initiative to demonstrate to your bosses that you add enough value to your employer to warrant an increase. You must first prove that you are a top performer before asking for more money. Start working on being on the company's best performers list if you haven't already. You should communicate with other top performers or the boss. Your boss will assist you in identifying important success metrics for your job. You can prepare yourself for a significant promotion if you can reach at least three trackable indicators in a few months. Find a better Company to Work forNot every company will recognize your worth. People used to toil for the same company for more than thirty years in exchange for a pension. Pensions, on the other hand, are almost gone, as the vast majority of employers have a 401k plan for their workers. Switch companies if you believe your current employer does not adequately compensate you for the work you do. It's better to discuss a bonus with the new employer because you have options. And if you do not wish to move companies, if another organization has an available vacancy, interview and establish contact with the human resource staff there. Shift CareersIf you're not being paid what you're worth, a career change may be the next best thing. Though change can be frightening, we won't be able to reach our full potential until we take a few measured risks. Embracing change and stepping outside of our comfort zones will pay off. Consider your talents and interests and how you can use them to the best use possible. Commence a BusinessA company will help you supplement your income and savings. You may launch a variety of small businesses in your neighborhood or online. Begin small and gradually expand your company. If you do have loans, the company will assist you with repaying them. There is no one-size-fits-all business; find out what your neighbors require and provide it. The first law in business is to fix problems for people. You should start a recycling company in your community if people in your neighborhood have trouble recycling plastics. Being an independently wealthy individual is a glossy option; however, remember that there is less of a fail option, but it can be overwhelming without proper consultation. We aimed to provide as much erudition as possible but to ensure that every point is clear to you, visit Atlanta Credit and book an appointment with financial consultation service experts today. Source:- Learn and Become Independently Wealthy

0 Comments

A personal loan is a lump amount of money lent by a bank or other financial entity that can be used for almost anything. What Is a Personal Loan and How Does It Work?A personal loan is one that you can get depending on your credit score and salary. Since no collateral is usually needed to fund a personal loan, it is often known as a signature loan or an unsecured loan.  The asset that can be taken and sold to repay the debt is known as collateral. The house being lent serves as collateral for the loan. Lenders usually accept personal loans based on their creditworthiness. As opposed to home and car loans, personal loans are comparatively simple to apply for and qualify for. As a consequence, they can be employed for everything from minor home renovations to large transactions. You can use the money on absolutely everything, but just borrow as much as you need—and just for anything that can help you boost your savings or have a significant effect on your life. How Do Personal Loans WorkWhen you have a personal loan, you usually get the money as one lump sum and repay it over time with fixed recurring payments. However, the specifics differ from lender to lender, and there are a few things to consider. Interest RatesYour interest rate is circumscribed by your credit score, which could be lower than that of a credit card. You might be able to borrow in the single digits if you have excellent credit. The interest rates on personal loans are usually fixed. The total interest rate remains the same over the term of the loan; so you'll have the same monthly payment. They may also have variable prices, but this is a less common choice. For a variable rate, based on whether interest rates are rising or declining, you can end up paying more or less interest. You could be charged rates that are close to credit card rates whether you have a short credit history or poor credit. A creditworthy cosigner may also be needed for the loan. Repayment TimePersonal loans are often repaid over one to five years, although other terms are available. As opposed to credit cards, personal loans will help you save money on interest and give you a specific payout deadline. There are no prepayment penalties on certain personal loans, meaning you can pay off your debt early and save money on interest. Make a monthly payment calculation.A personal loan's monthly payment is determined by the loan's number, duration, and interest rate, highly dependent on your credit score. Fees for OriginationMost lenders charge origination fees for personal loans, while others include all charges in the interest rate. Your lender takes an upfront payment depending on the sum you borrow when you pay origination fees. Origination payments usually vary from 1% to 8% of the loan volume and are determined by the credit score. Fees are mostly deducted from loan payments, meaning you get less than the entire loan sum. To pay the tax, make sure you borrow slightly more than you need. How to Get Approved for Personal CreditCreditworthiness is used by lenders to assess loan applications. These are the things they usually think about. Credit HistoryLenders also review your background or obtain a credit score to learn about your credit history. Your credit reports provide information about recent transactions, missed payments, and public documents that lenders may be interested in. Lenders can also use alternative credit scoring tools. To assess how you'll repay a loan, they might look at your history of on-time rent and utility payments, for example. IncomeLenders must ensure that you have sufficient income to repay the loan. They will inquire about your jobs and earnings. They might even peek at your existing loans and see if adding a loan payment would eat up too much of your monthly revenue. Personal Loans: Different TypesIf you plan to take out a personal loan, you have some options. Credit UnionCredit unions are expected to offer low-interest rates. If you need money but have bad credibility, credit unions are a better choice, and they are more likely to work for you. Assume you want to become a member of a credit union. Under any case, you'll need to meet such affiliation criteria, such as residing in a specific geographic area, working with a specific employer, or paying a subscription fee to a third-party organization. A credit union savings account can also encourage you to keep a certain amount of money. BanksCredit unions charge lower interest rates and have stricter lending requirements than banks. However, since banks do not have the same membership restrictions as credit unions, it's still worth considering what they could do. Furthermore, the issue with bank loans is that they have a lengthy approval period that can take anything from one to two months. As a result, if the needs are urgent, it is not the best solution. Personal FundersIt usually is simple to apply for a loan because many online lenders have swift approval and deposit times, even as soon as the same day. However, don't let the ease of instant cash stop you from looking for better deals; these offers can seem to be attractive, but they conceal secret flaws. If you are keen on funding your private endeavors without any fear of dirty deals, you need to visit Atlanta Credit Experts. They have fair interest rates with no hidden cost and customer efficient services ideal even for finance naive. Spending a Personal LoanA personal loan allows you to spend the money on virtually anything you desire. Debt ConsolidationIf you owe a balance on credit cards with high interest rates, you will pay them off with a lower-interest personal loan. Since less of each monthly contribution goes toward interest rates, you can pay off debt faster. Home Improvements on a BudgetSince you're reinvesting in your house, it's normal to use home equity loans for home improvement projects. However, if you don't need a large sum, a personal loan for home renovations can be less costly and quicker to obtain. Expensive PurchasesWhen you need to buy something extensive or costly but don't have the funds, a personal loan will be able to help you. Putting Money On YourselfWhen you need to start a company or develop new skills for your job, personal loans can be able to help. However, some lenders have restrictions on how you can spend the money you borrow. Some personal loans, for example, do not allow you to use them to pay for higher school costs. Situations That Need Immediate AttentionYou should have emergency funds set aside in case life throws you a curveball. However, there are periods where borrowing is the only solution. A personal loan could make sense if you're facing large medical bills or some emergency. Important Points to Remember

TABLE OF CONTENTS

When it comes to planning for education, students must weigh all the financial assistance options. Scholarships and grants are the preferred types of financialassistance since they are non-repayable and can be called free money. Even with scholarships and federal loans, most students will face a financial deficit in their education fund that will necessitate using a student loan in any manner.  If you take out a federal loan or a private lender loan, there are advantages and disadvantages to remember for all student borrowers. A loan of some sort is a significant financial commitment, and a well-informed student would be in a much stronger position to find the best loan deal possible.

Plain Good Deals on College Loan Terms Many citizens are rightly wary of taking out a loan. Any loan is a big commitment and, therefore, must not be treated seriously. However, student loans are often required in order for a young person to pursue their college aspirations. Student loans, fortunately, also come with special conditions and circumstances that make them reasonable and realistic for a young student who wishes to pursue future studies. Most college loans have lower interest rates, graduated payment plans, i.e., a grace period until graduation for repayment. Unlike the more stringent terms and conditions of a regular loan, student borrowers may take advantage of more lenient repayment arrangements and timelines exclusive to school loans. College Student Loans Are FlexibleStudent education loans are more flexible and have more reasonable terms and conditions than traditional non-education loans. Both federal and private lenders are aware of the demands of a college degree and, therefore, work to make college loans more manageable for students. Federal tuition loans are perhaps the most flexible, as they allow their borrowers to access much-needed educational funds in very favorable terms. Federal grants are awarded based on financial necessity, and almost all campus students will qualify for a kind of government loan. Students still studying in colleges can reap the benefits of federally funded schemes such as the Stafford Loan and the Perkins Loan, which offer reduced fixed interest rates and deferred payment plans. The Federal Direct Stafford Loan is a highly appealing program because it provides qualified borrowers with a subsidized alternative. The federal government will reimburse all accumulated interest on a guaranteed Stafford Loan for as long as the student is enrolled in college. Student loans from private lenders will be as versatile as those from the federal government. They have more advantages than a traditional non-education loan. Personal loans are determined based on an applicant’s financial background. But here, most students would need the assistance of a cosigner, also known as a co-borrower. A parent or legal guardian is usually the one in charge. Having a cosigner is beneficial in two ways. It enables the student to obtain a loan with lower interest rates and more favorable repayment conditions, and the ability to establish his or her own credit history. Furthermore, college loans from private lenders often have lower interest rates than public loans and have loan deferments, which enable borrowers to defer payments until after graduation. Keep in mind that all private student loans continue to accrue interest during the deferment time. Low Fees on Student LoansFinancing directly from a student loan specialist comes with its own set of advantages. Student loan lenders create loan programs tailored exclusively for their student customers, tailoring their goods and services to college students. Private student loans for undergraduates and seniors are often accompanied by hidden costs. As a means of enticing borrowers, a private lending company will usually pay reduced fees. Any banks and student loan agencies will also suspend origination fees and early repayment fines altogether if a student borrower meets such criteria. Customization is not permissible for Federal Family Education Loans or Federal Direct Loans. A series of rules govern this federal loan initiative to guarantee that all student borrowers are handled equally. There are no origination costs for federal loans, and there are also no fines for repaying them early. College Loans and Low-Interest RatesA hidden advantage of borrowing from federal student loans is that they have reduced fixed interest rates. The terms are fixed for the loan duration and are typically the lowest available for an education loan. So while in a quest for college financial assistance, college-bound borrowers can look at federal loan services to obtain the most attractive and manageable loan arrangements. Depending on the lender and the specific loan arrangement, private lender loans may have different interest rates. Since all personal loans are based on a borrower’s credit score, private lenders adjust interest rates accordingly, with the lower the interest rate, the higher the credit history. By enlisting a consigner’s assistance with a strong credit background, student borrowers will lower the interest rate on their loans. Good lending habits will also result in lower interest rates throughout a student loan’s existence. Student Loans and Borrower IncentivesTo draw customers, most banks and private banking organizations may provide borrower offers. These incentive programs also target education loans, which will help student borrowers save money while applying for and obtaining a personal lender loan. Following are some of the most famous reward programs:

Conclusion Education is a costly endeavor, and most students would need to take out some form of education loan to help cover their overall costs of attendance. Do read the fine print while considering an education loan, whether from the federal government or a private provider. Do your homework, consider the benefits and drawbacks, and never sign something until you’re sure you understand and feel satisfied with all of the terms of your college loan. If you need to learn more about college/ student loans contact Atlanta Credit Experts. They will provide you a loan at affordable interest rates perfectly suited for your needs. Source:- BENEFITS OF OPTING FOR STUDENT LOANS Customer acquisition for credit card companies has evolved into a rat race in which even the tiniest chances to attract customers are not overlooked. Pre-approved credit cards are an example of this. If you check every email we are sure that your inbox column would have at least two to three offers of such credit cards from three to four different banks. These deals are received by almost all of us. But what exactly should be done with these offers? Should we condemn them outright or do we go for it? But do you know that between the hasty acceptance and rejection decisions, there is another path to take: information and study. Keep reading to understand the hidden reality of pre-approved credit cards, the advantages, repercussions, and misconceptions surrounding the same.  Be Doubtful, Not Debtful

It’s important to first understand the product, its flaws, and what it can do for you in the long run. Credit cards are so widely available these days that it’s tempting to ask if shopping with a plastic card is more addictive or other narcotic addictions. The reality is that every highly beneficial product has a flaw that, if exploited, can leave us in a ditch. So, before you get one of these pre-approved credit cards, hang on and learn a little about them. What is a Pre-Approved Credit CardA pre-approved credit card will be offered to you by your credit card issuer or bank. There is no guarantee that you’ll get it. In fact, it means that the credit card company or bank has combed through CIBIL score databases and the list of people who are qualified for a credit card. As a result, an automated mailer is sent to people with high CIBIL scores as a lure to bait you in as a customer with a pretty worm known as a pre-approved credit card. If you proceed, the bank or credit card agency may perform another round of credit history evaluations. If they do not deem your credit history to be satisfactory, your application will be refused, potentially lowering your CIBIL score. If your application is refused, you will end up taking two steps backward. Can Pre-Approved Credit Offers Be Further Hazard?Here are several reasons why you should think twice about applying for additional credit cards, regardless of how good your CIBIL score is:

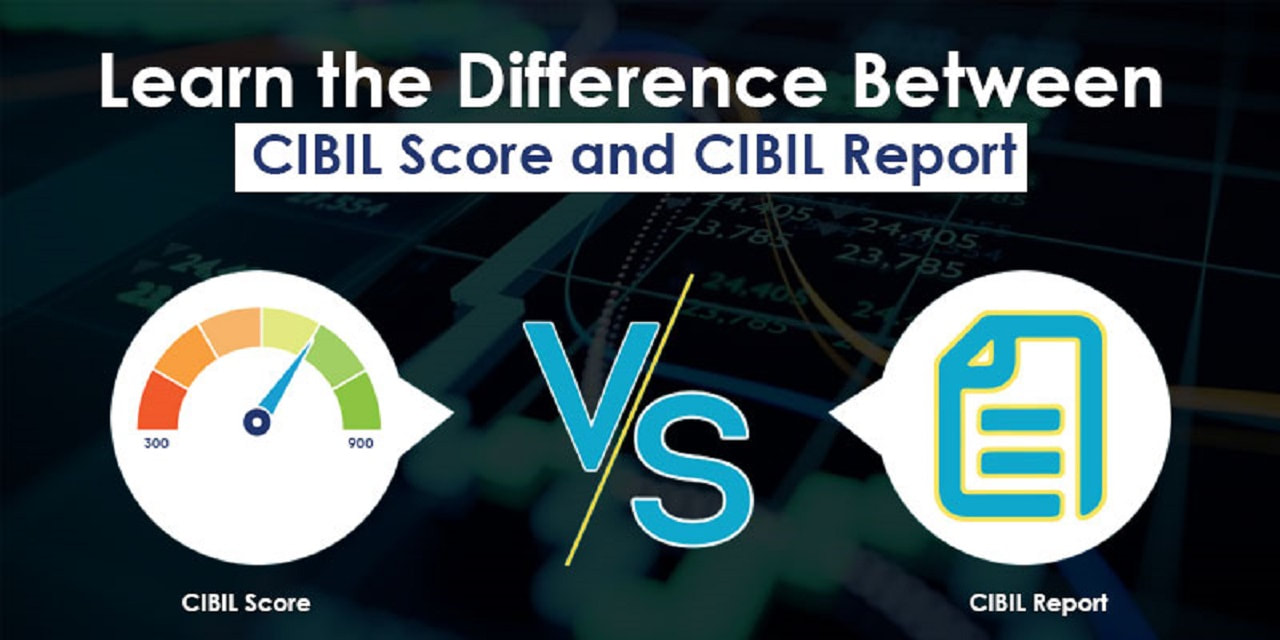

Credit Card Misconceptions Among People There are certain misconceptions that people hold. They don’t actually know the real reason and logic behind the situation. We took it on ourselves to clear their misconceptions and provide them with factual and logical explanations. Misconception 1: It Isn’t Good to Have Multiple Credit Cards. One of the main worries about getting multiple credit cards is the effect on your credit score. This is a common concern among people. They fear that if they apply for multiple credit cards, it will adversely affect them. The fact, however, is that owning multiple credit cards has both positive and negative effects. However, getting multiple credit cards will actually improve your credit score by making it easier to maintain a low debt utilization ratio. For instance, if you have one credit card with a $2,000 credit limit and spend $1,800 on it on a monthly basis, your debt utilization ratio, or the percentage of your usable credit that you use, is 90%. When it comes to credit ratings, a high debt usage ratio can lower your ranking. It might not seem fair—why should you be penalized for using the majority of your credit limit if you only have one card and pay it off in full and on time every month? But that’s how the credit score system works. But understand if you don’t have such high usage and have multiple credit cards, it will adversely affect you. Your debt utilization ratio will be low, and the yearly/ monthly fixed bills of the same will be high. Misconception 2: Credit Utilization Doesn’t Play a Role in Credit Cards It is rightly said that it is a misconception because it is one of the essential determinants. Therefore, one must keep their credit line utilization ratio below 30% and stay on top of payment deadlines. Most credit experts advise against using more than 30% of your available credit per card at any given time in order to increase your credit score. It’s also easier to keep your credit utilization ratio down by spreading your $1,800 in transactions across many cards. This ratio is only one of the variables considered by the FICO credit scoring model in the “amounts owed” part of your ranking, but it accounts for 30% of your total credit score. Only 35% of your payment history is taken into account when calculating your credit score. FAQ’s How Many Credit Cards Should You Have?People usually come up to us and ask how many credit cards are the best options. Now there is no magic number to that question because everyone’s situation is different. A strong argument can be made to have at least one credit card to take advantage of the inherent convenience, security, and other benefits. If you need the extra credit lines to accommodate your monthly spending budget then the demand and requirement of credit cards are justified. Alternatively, if you want to use your daily spending you can collect incentives such as cash backs, points, or airline miles. How Many Credit Cards Are Too Many?The answer to such questions is never definite. For some people, even getting two credit cards can be excessive. Remember, if you can’t afford to pay your bills, you don’t need them and therefore refrain from using them. Getting a new credit card will help your credit score by lowering your overall credit line usage, but getting many cards in a short period is not recommended. Many card issuers have rules in place to address this practice, which has emerged as a result of consumers attempting to cheat the system by signing up for several credit cards in order to collect incentives and then canceling after the spending criteria have been met. For example, Chase, America’s leading bank, has a policy known as 5/24, which states that if you’ve applied for more than five credit cards (regardless of the issuer) in the previous 24 months, you won’t be eligible for anymore. Another such disadvantage of getting a large number of credit cards is that it can make you seem risky to lenders, lowering your credit score. Even if you’ve paid them all off, the simple fact that you have a lot of open and unused credit lines will make you appear to the next lender as a possible liability. Although there is no absolute limit on how many credit cards you can get, it’s better to apply for and hold only the cards you need and support using based on your credit scores, willingness to pay balances, and rewards goals. Should We Carry Credit Cards for Emergencies?According to us, it would be ideal if you didn’t need to use your credit card in an emergency and instead had enough money in a liquid account, such as a savings account. When you’re on holiday and don’t have enough money to cover a car repair or some form of unexpected cost when you’re away from home, a credit card can come in handy. Other circumstances, such as an unexpected medical bill or losing your work, can quickly deplete any emergency savings, so getting at least two or three credit cards can come in handy in a pinch (the present Covid-19 pandemic being a good example). These cards should ideally have no annual charge, a high credit limit, and a low-interest rate. Conclusion Our final thoughts on the hidden reality of credit cards are that using many credit cards has a lot of advantages, but only if you use them responsibly. So, be aware of the benefits each card provides, the credit limit on each account, and, most importantly, the payment due dates to ensure that having multiple credit card accounts works for you rather than against you. Be aware of all marketing grimaces and take help from credit experts from an organization running for your benefit. If you didn’t find anyone worth your trust, come to Atlanta Credit Experts and get the solutions to all your financial worries. Source:- Hidden Reality of Credit Cards Entrepreneurship of big or small corporations, even in favorable times, is challenging. The small business credit survey conducted by the Federal Reserve system in early 2020 indicated that 57% of the total small businesses enjoyed profit, and only a margin of 24% operated in losses. The figures took a considerable downfall when the lockdown period began. The same researchers showcase that the small business holders were railroaded. They only had a cash flow suitable to support one-month operations, leaving both the business owners and employees vulnerable to face pandemic consequences.  Clearly, the global recession period of 2020 ended good times for small business owners. Due to reduced revenues and lack of financial support, numerous businesses fought for their survival, out of which many couldn’t survive the day. No matter how hard it was for the existing business owner, the pandemic gave us ample time to find ideas to venture into their desired fields and open businesses. The pandemic’s consequences are panning out, and with tons of financial organizations available in the market, it is an ideal time to water your dreams and grow. If you wish to fund your dreams, ensure that you know all the right and wrongs available in the business and all financial needs to flourish your vision in reality. To help you with the same, we are listing a few pointers you need to keep in mind. How will you fund your business?If you are on the voyage to open a small-scale business unit, you need to ask yourself how you will fund your business. Do you have a deep pocket that will support you for months or years of break-even? If not, what are your alternatives? These questions will allow you to understand that your needs require financial assistance. You need to take the help of credit experts who are ready to share your risks with you and help in driving your capital forward. The ideal choice for funding your dreams are Atlanta Credit Experts; these professionals will push your operations forward and will ensure that you have the desired working capital and resources to support your way in the financial world. They will ensure that you fund your business using alternatives that will prove beneficial in the future and won’t degrade your image. The financial experts are also pro’s in getting you access to even personal funding options. Do you have the desired credit score?As a new player in the market, it is understandable that you might not have the desired business credit score or satisfactory personal credit options. The problem can be avoided/dealt with if you are planning your operations thoughtfully. The primary prerequisite of credit funding is the credit score. And whether you wish to avail yourself of business funds or personal funds, you need to have a stabilized score. Usually, people are unaware of their CIBIL or credit score that imposes consequences in their future financial endeavors. Read also: Preparing Teenagers for Good Credit Score For funding small businesses, the entrepreneurs must remember to keep a check on their credit scores. If they have a low or degrading credit ratio, they must immediately take credit repair experts’ help. Financial experts available in Atlanta Credit will ensure that you have a satisfactory credit score to avoid every financial obstacle that might come in your way of getting approved. What is your plan after you get business funds?After you have successfully understood what funding solutions you will rely on and how you will derive the desired credit score, you need to lay your mind on how to get your vision to practice. After reckoning business owners’ concerns on how to drive the credit they received, Atlanta Credit Experts have come up with a unique credit consultancy service. The financial experts provide their corporate clients proper knowledge and inspiration for analyzing the customers’ business model. They advise you with the right plans and strategies to allow its customers to bag all the success under the roof. The top advantages of Atlanta Credit Experts are that they provide A to Z Credit Consultancy with analytical planning and streamlining cash flow. The financial experts also provide complete financial Assistance and capital risk reduction measures. To sum it up, we believe that every new business owner, regardless of how small or big a corporation he acquires, requires capital and cash flow to drive their operations forward. The primary prerequisite of getting approved for credit is a stabilized credit score. Furthermore, to ensure that their vision works in sync with their funds, business people need reliable guidance. To avoid all these concerns/problems, Atlanta Credit Experts are the able solution. The professionals will ensure that you grow your small business and bag success by avoiding all obstacles that might come your way. Visit Our Site:- Grow Your Small Business with Atlanta Credit Experts Your CIBIL Report is a comprehensive record of your credit history that includes personal data, contact information, job information, loan account, and credit card information. CIBIL Score, on the other hand, is a three-digit statistical overview of your CIBIL Report that reflects your creditworthiness. This is focused on your credit history and payment habits, which is an integral part of your profile because most creditors use your past behaviors to predict your potential behavior.  Your CIBIL score is a synopsis of the last 24 months of your credit behavior, whereas your CIBIL Report covers the previous 36 months of your credit history. Despite the variations between your CIBIL Score and Report, it’s important to remember that both play a role in your loan application’s approval, and lenders use both to determine your loan eligibility.

To be eligible for a CIBIL Score, a person must have more than six months of credit details. On the other hand, a new-to-credit customer may not have enough facts or credit history to produce a ranking. They may be given an NH/NA in this case (No History or Not Available), allowing them to develop their credit footprint over time by practicing good credit habits like timely repayments, a diverse credit mix, and remaining within their credit utilization limits. This will ultimately result in a statistical CIBIL Score ranging from 300 to 900. The higher your credit score, the more likely your loan application will get accepted. In reality, consumers with a CIBIL Score of 750 or higher are approved for 79 percent of loans. Read more: Build A Best Positive Credit Score for Personal Funding Loans If you are novel to the credit world and don’t have a considerable score yet (or don’t have one greater than 750), there is no need for you to lose heart. Fortunately, some lenders might not even look at your credit score; instead would check your CIBIL report for an extensive view of your credit footmark. Here they will seek to check the date past due on your owed payment and whether or not you have any red flags on your loan accounts. Another important consideration here is the number of inquiries set on your account because every one of these details is available in your credit report. The CIBIL Report’s information allows the creditors to determine how risky a deal they are underwriting and whether they should approve your loan application. Furthermore, for the past couple of years, selective banks and credit lenders have come up with policies that reward credit-conscious and high-scoring customers. The banks reward such consumers with privileges on pricing loans (with discounted interest rates). So, reckon that a high CIBIL score or healthy report will ultimately allow you to access credit easily as well as will pave your way for considerable savings. If you want to accomplish your financial goals, you must aim for a CIBIL Score equivalent or higher than 750 with a polished CIBIL Report. Regularly checking your score and report allows you to ensure that your personal and loan account information is up to date, ensuring that you have access to credit when you need it most. Everything aforementioned gave us a fair idea that our CIBIL score is a highly vital variant. It is the first impression lenders look at while appraising any loan application. Therefore it is important to learn how to calculate the desired score. Calculating your credit score is a hefty task that requires a proper proprietary algorithm. Apart from all the statistical appraisal records, the other important element that one needs to keep in mind while calculating the score is one’s loan payment conduct. CIBIL ScoreThe CIBIL score is a three-digit numeric overview of your credit history. It is calculated using information from your CIBIL report’s ‘Accounts’ and ‘Enquiries’ pages, which includes (but is not limited to) your loan accounts or credit cards, payment status, and outstanding amounts’ days past due. The score reflects your creditworthiness, as determined by lenders, based on your borrowing and repayment history. CIBIL score varies from 300 to 900, where the higher your score, the more likely you are to be accepted for a loan. In reality, consumers with a CIBIL score of more than 750 are approved for 79 percent of loans. How is the CIBIL score calculated?CIBIL score derives its analysis statistics from four key factors.

Credit ReportCIBIL reports are a thorough analysis of a customer’s credit history received from lender and bank entities. The entire data obtained is then processed and formatted in the form of a detailed report. Read below to understand the commonly contained elements in the CIBIL report.

ConclusionIdeally, customers should avail of their credit report/ score synopsis once a year to ensure that all the information stated is free of discrepancies. But where to obtain a reliable credit report? If you wish to seek credit reports, the first option available here can be applying for CIBIL accounts online. The other option available here is pounding all your credit worries on a financial company like Atlanta Credit Experts. The company will help you with the best financial advice that will allow you to obtain the best credit score and ultimately get approved for funding. Navigate to Atlanta Credit Experts official website and learn all the ifs and buts of the financial world. Source:- Learn the Difference Between CIBIL Score and CIBIL Report After viewing the staggering figures of student credit loans reaching $1.56 trillion in 2020, a practical individual just can’t help but wonder how much student loan will affect his/her credit score. We all understand that a student loan is installment solvency, and therefore like every other loan, they directly affect our credit score. Both loan and credit score are directly related to one another hence their operational direction is in our hands.  Clearly, we understand the primary aspect of this relationship. Still, the question arises that does student loans have only a positive impact on your score, or can they impose any adverse effects? After analyzing the direct impact on credit score, understand if credit scores can impact your student loans? You don’t have to look for valid answers anywhere; instead, read the information given below to understand all the ifs and buts of this correlation. In-Depth Analysis of Student Loans and Credit Score CorrelationTo understand student loans’ effect, you need first to understand the primary aspects of credit score. So let’s begin by reckoning what comprises a credit score. These financial debt tabs are nothing but a large portion/proposition of your loan repayment history. It is an account that mirrors your first impression to the lender, and based on this; they formulate your image of whether or not you are a safe borrower. These reports comprise 35% of your total score and contain figures about how regularly/irregularly you paid the installments over the due course of your loan. These payment histories then serve as a piece of evidence to determine how sincere you are as a borrower. As student loans fall under the category of installment loans alongside asset loans, its tab does reflect on the individual’s payment history. They fall under the category of loans that affect 35% of your total score, and any late/missed payment does stay put a time span of seven to ten years. Can Paying Student Loans Build Credit Score?Similar to every other loan, timely repayment of student credit does positively reflect on credit score over time. The benefit might be minuscule, but every aspect that doesn’t harm your credit score is worth noting. As stated above, loan payment history comprises 35% of your credit account. Therefore paying loan installments in a timely manner reflects positively on your accounts. Apart from payment history, two other factors forge your accounts into what they are today.

How Can Student Loans Hurt Credit?As discussed above, student loans can be beneficial for your credit score. But the question arises that can these loans hurt your credit score? Yes, it can, and let’s see how. We reckoned that paying our installments on time constructs a very reliable image for us then if you miss a payment, the effect will deteriorate your picture. The payment history of student loans stays on your credit report; hence, lenders will refrain from approving your loan if you have a poor record. These consequences of defaulting on a loan can be avoided if you cover the tracks of your missed payment soon. The reporting time frame solely depends on how early you fix the situation and the type of student loan you have acquired. Suppose you have funded your education from a traditional banking entity in the form of a federal loan. In that case, they report the problems to the three major bureaus (Equifax, Experian, and TransUnion) after 90 days of default. On the other hand, if you have taken a loan from a private lender, they usually wait for 30 days, or the payment failure is reported to the federal bureaus. Another reason that can degrade your credit score is if you apply for a loan from an untrustworthy private organization. They will conduct a hard pull on your credit report that will spoil your credit process. The last factor that can harm your credit score is borrowing an amount more than needed. As you are a new player in the market, it will increase your debt to income ratio, which ultimately will cause your score to go down. If you wish to understand more on similar lines or are looking for institutions that can help you repair your credit score, contact Atlanta Credit Experts. They will provide you with out-of-the-box options for personal and business funding with proper guidance to avoid every potential financial obstacle that might hamper your success in the future. Source:- Effect of Student Loans on Credit Score Atlanta Credit Experts believes that everyone has some kind of goals and dreams in their life, and the goals and dreams will remain a dream if they don’t receive effective persuasion to achieve them. Therefore, with careful financial planning and better management of assets, the company wants its customers to achieve their dreams efficiently. Our professional understanding and assistance will make your plans easy and effective.  In other words, if you want to achieve what you dreamt of without having to undergo obstacles, hire a financial credit consultant.

Who are Atlanta Credit Consultants?Atlanta financial consultants or planners are monetary experts who will provide you credit consulting services and advise or assist the clients in opting for the most desirable loan option. The Atlanta Credit Experts will help you bridge the gap between your business plans and walk to the bank to settle the credit score. The Atlanta Credit consultants’ primary aim is to ensure that the modern-day business-man or woman never let the factor of under-capitalization ruin their business servicesor create any unforeseen hindrance in their potential success. The company is known to provide one of Atlanta’s best credit repair services. Therefore, whether you are heartily working on the next big thing in your backyard or building a world-class retail store, you will have a balanced control over your operational cash flow. If you want to bag success, you should have an expert eye for detail or hire an expert from Atlanta Credit to help you with it. How Does Atlanta Credit Experts Provide Financial Advice?The financial consultant typically carries out a wide range of steps so as to provide reliable assistance. The steps are as follows.

The Atlanta Credit Experts possess all these qualities and hold a good command over mathematics, computers, statistics, and business service requirements. The company has top-notch customer service and promises accuracy, trustworthiness, and honesty in its operations. Core Advantages

Phone: +1 404 940 2166 Email: [email protected] Headquarters: 3355 Lenox Rd NE, Atlanta, GA 30326 Source:- Credit Consultancy Business Services By Atlanta Credit Experts Every company, big or small, needs funds to operate. For paying salaries to thousands such everyday operations, they need stable cash flow support. The deep pockets might come in handy initially, but with time to drive the work forward, one needs credit support. The monetary aspect for once can be managed by seeking help from here. It might make you survive in the market for considerable years; eventually, your steps can flicker without proper credit guidance. Therefore it is often suggested that before opening a business, one must create a blueprint to ensure that you don’t miss any unexpected opportunity that can bring great returns due to lack of working capital.  There is a possibility that you might understand the need for business funding but don’t know which organization to approach. As there are tons of companies running to provide you funds and credit consultancy, it can be easily confusing. For getting the best solutions to all your funding and consultation worries, you must contact Atlanta Credit Experts. To understand how the company operates and the advantages of Atlanta Credit service, carefully read the information stated below.

Business FundingAtlanta Credit understands that every business, big or small, requires working capital to drive forward, and we, therefore, provide fast and straightforward business funding options. To ensure that no one lets go of a successful venture due to financial constraints or delay in operations, we have kept our application process for business funding extremely simple and immediate. When you apply for business funding with Atlanta Credit Experts, you won’t incur any wrongful origination fees, hidden costs, or processing fees. We take immense pride in saying that our organization understands business’s struggle, and therefore we run our operations with utmost honesty and accuracy. To help you get the best of services, Atlanta Credit has whipped all the complications of funding a business. Furthermore, if you select Atlanta Credit experts, it will help you process your request in no time with a rewarding streamlined, and personalized experience. Core Advantages

We also provide information and inspirational insights to our clients to ensure that they possess the proper knowledge of all nitty-gritty before getting in the process. Atlanta Credit Experts are aware that every business is distinctive from one another, and therefore, we provide insights by studying every little detail of the business. After formulating a report on the company’s details, we act as a catalyst to understand the shapes and sizes to reduce typical risks associated with credit and capital. To sum it up, Atlanta Credit Experts will help you bridge the gap between your business plans and walk to the bank to settle your credit score. We comprehend that it is your time to become the face of tomorrow, and the sole fact of under-capitalization mustn’t ruin the business model or create havoc in your potential success. We are known as one of the best credit providers and consultants in Atlanta. Core Advantages

Source:- Business Funding and Credit Consultants By Atlanta Credit Experts |

AuthorWrite something about yourself. No need to be fancy, just an overview. ArchivesCategories |

RSS Feed

RSS Feed